2023 Retrospective

Clean energy stock performance was dominated by macro factors in 2023, especially interest rates. The U.S. 10-year Treasury yield reached a high of 4.99% in October. The performance of clean energy was also impacted by sector-specific factors. Notably, solar companies faced an oversupply situation in Europe that was exacerbated by lower market power prices and higher interest rates.

Despite the macro headwinds, there were some positive signs. Many companies managed through the higher interest rate environment by capitalizing on lower equipment costs, which were helped by easing supply chain constraints. Despite higher interest rates, companies reaffirmed order backlogs and return targets, which is evidence of the continued strong demand for clean energy. Lastly, while still in the early phases, elements of the U.S. Inflation Reduction Act (IRA) are beginning to be put to work, including tax transferability, which is proving to be an efficient funding mechanism for renewable developers.

2024 Outlook

The macro backdrop signals interest rate cuts as early as the first quarter of 2024. While lower rates would provide a boost to clean energy valuations, we should also be careful of what we wish for. Rate decreases may also be the reaction to real economic deterioration, which isn’t necessarily positive for equities. Despite this variability, the clean energy sector maintains attractive long-term investment characteristics where we can capitalize. The strategy continues to position in businesses that are not solely dependent on the direction of rates.

Industrial expenditures in clean energy continue to gather momentum. U.S. utilities are bumping up capex, with more spend dedicated to renewable power while addressing grid upgrades. Put simply, renewable capital deployment continues to be viewed as both profitable and necessary. Numerous state governments including Michigan, New York, and Colorado are adjusting and adapting to the macro realities in order to continue renewable deployment. Unlike the industrial and utility segments, residential consumers may take more time to adjust. We believe residential solar may start to see a more meaningful recovery in the second half of 2024. Finally, in the U.S., the IRA remains key and has led to a pickup in clean energy investment activity, with more to come as the U.S. Treasury provides increased clarity on tax incentives regarding domestic content, energy community, section-45X credits, and other technicalities. The U.S. presidential election and the prospect of a Republican win brings concerns for potential changes to the IRA, but we believe the likelihood of a complete repeal is quite low. Even so, we will be watching for any potential reconciliation bill, especially if Republicans look to extend the Trump tax cuts, which expire in 2025.

In Europe, the ‘energy crisis’ has subsided and with it regulatory and political intervention risks for the continent’s main renewable developers. Still, the energy transition remains top of mind in order to ensure adequate resources. The need to grow renewable power and promote electrification will also require substantial upgrades to grid infrastructure. Several actions were taken across the EU to support clean energy deployment including fast-tracking renewable permitting, improved offshore wind support, and an ambitious power grid overhaul plan. Local and country-level action also continues. In sum, like the U.S., Europe is adjusting and adapting to certain macro realities in order to maintain clean energy momentum. We expect more EU countries to formulate and adopt accommodative clean energy policies, with Germany the one to watch in 2024. Politically, Europe is more nuanced and in need of energy independence. This explains why a modest turn to the political center-right for the EU following recent local elections does not alter the continent’s path. However, more resources could potentially tilt to nuclear (country-specific) and greater localization of clean energy equipment manufacturing within budgetary constraints. Overall, though the political landscape in the EU could shift in 2024, the economic case and geopolitical need for clean energy remains.

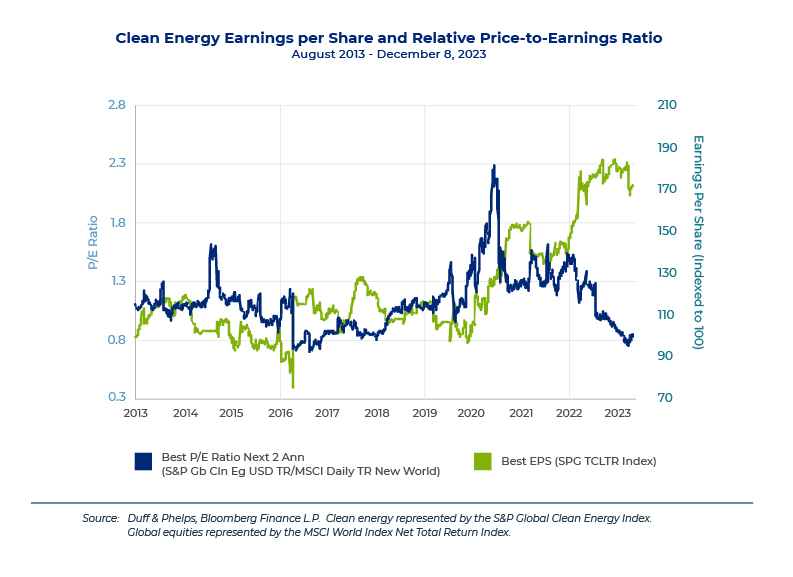

Market volatility has allowed us to find investments that we believe will endure through the energy evolution. In fact, clean energy valuations are the most attractive we have seen in years, see the graph below. Paired with earnings estimates that remain in a rising trend, compelling equity opportunities continue to emerge. This highlights the importance of active management for clean energy investors. The world will continue to evolve toward safer, more reliable, and cleaner energy. The Duff & Phelps Global Clean Energy Strategy seeks to invest in businesses with strong growth outlooks, scale to maintain pricing power, and the ability to generate attractive returns.

This material is for informational purposes only and not intended as investment advice or a recommendation to buy or sell any security. Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within Duff & Phelps Investment Management Co. Information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented. Investing involves risks, including the possible loss of principal. Duff & Phelps Investment Management Co. services are not available in all jurisdictions and this material does not constitute a solicitation or offer to any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation.