2023 Retrospective

Interest rates and the future of inflation were major elements of uncertainty at the start of 2023. As the year commenced, the same question we face today was top of mind. That is, could the U.S. Federal Reserve (the “Fed”) and its central bank peers engineer a reduction in inflation without causing too hard an economic landing, and how would that impact real estate? It was clear to us that inflation momentum would play a significant role in determining investment returns for listed real estate.

Having assessed this, and noting a volatile interest rate environment throughout the year, we remained focused on and committed to investing in companies with strong balance sheets, clear growth potential, and stable cash flows. As real estate investors, in addition to this steady focus and commitment, we have continued to closely and continuously evaluate whether real estate companies would be able to operate efficiently and grow cash flow and income in the current environment.

At the beginning of 2023, it was the market’s view that the Fed would cut rates in the second half of the year, though we believed it would take longer to reduce inflation, and that the Fed and its peers would demonstrate patience. It was arguably the bond market’s notable decline from the end of the summer until the end of October on solid employment growth, as well as resilient consumer spending, that made the patience we anticipated and observed in practice possible. Treasury yields rose to levels not seen since 2007. And it was this window that set the stage for the rally underway in listed real estate.

Looking at the underlying country performance across the listed global real estate markets, through December 19, 2023, we saw a reversal from 2022 with Western Europe outperforming Asia-Pacific and the U.S. ahead of the overall benchmark. Germany, Austria, and France led within Europe, and Hong Kong, South Korea, and Singapore lagged within the Asia-Pacific region.

On a property sector basis, nine of the 11 global sectors delivered positive total returns on the year, a significant improvement from 2022. Data centers were the clear winner, delivering returns greater than 28%. Data center demand and pricing power benefited from the material increase in artificial intelligence-related workloads, leading to record-breaking leasing in many markets. Lodging and industrial were the next- best-performing property sectors. The diversified, specialty, and office property sectors were notable laggards. Office continued to suffer from subpar utilization, more so in the U.S. than internationally, as employers continued to adjust their workplace strategies and associated future office space demand needs.

Cash flow and dividend growth for listed global real estate companies remained positive, but did experience downward earnings revisions as we expected, driven by higher operating and interest rate costs. Public-to-public and privatization merger activity continued, particularly in the U.S., where we saw large-cap REITs buying their smaller competitors to enhance scale and platforms.

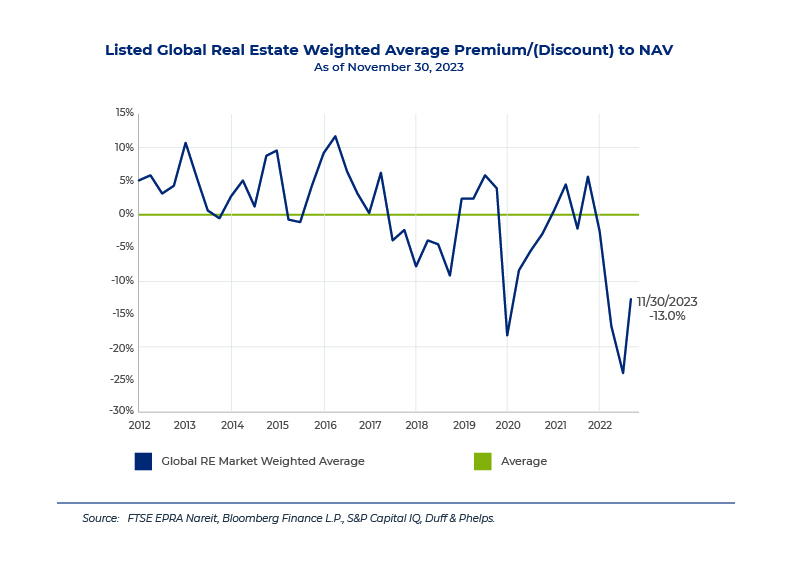

Through the time of publication, global listed real estate continues to trade at discounts to NAV estimates of private market valuations and, relative to history, is trading inexpensively vis-à-vis broader market equities.

2024 Outlook

The Duff & Phelps Global Real Estate Securities Team expects global economic growth to slow in response to higher interest rates and quantitative tightening. Unlike last year, in 2024 we expect the Fed to lower rates to curtail hard landing risk surrounding the November presidential election, which in our view will benefit listed real estate.

Naturally, just as we expect global economies to slow, we expect global listed real estate cash flow to remain positive yet decelerate across many property sectors, as companies absorb higher financial and operating costs. Quality and resiliency in the form of well-positioned balance sheets and sustainable growth in cash flow and dividends will likely be preferred by investors as we continue to face an uncertain economic environment.

Fundamentally, secular growth drivers should continue to benefit data centers and logistics. Within the U.S. health care property sector, senior housing operating properties and skilled nursing facilities will continue to see an improvement in occupancy. And pricing power should increase further in senior housing. Self storage has been impacted by the moderation in housing turnover caused by higher interest rates and, in certain markets, a higher level of new supply, which is negatively impacting pricing for new customers. The residential apartments subsector in the U.S. is also in the process of digesting a significant amount of new supply over the next 12 to 18 months. The office property sector will likely remain one of the more challenging and controversial sectors on a global basis.

Given the capital that has been raised by private equity sponsors on a global basis, the new year may see a pick-up in public-to-private M&A activity, particularly if debt availability and pricing improve and global listed real estate continues to trade at discounted valuations.

In our view, listed global real estate has shown an ability to outperform following the end of a rising interest rate cycle, and should clearly be a beneficiary of lower rates. With an abundance of private capital on the sidelines and discounted pricing available via listed real estate, arguably at wholesale prices, we see listed real estate as much more attractive than private real estate.

This material is for informational purposes only and not intended as investment advice or a recommendation to buy or sell any security. Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within Duff & Phelps Investment Management Co. Information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented. Investing involves risks, including the possible loss of principal. Duff & Phelps Investment Management Co. services are not available in all jurisdictions and this material does not constitute a solicitation or offer to any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation.